Practical Project Risk Management

SERIES ARTICLE

By Martin Hopkinson

United Kingdom

Purposes

- Manage contingencies so as to reduce the risk of cost overrun or margin erosion.

- Assign responsibilities for cost risk that are aligned with the project’s governance.

Typical approach

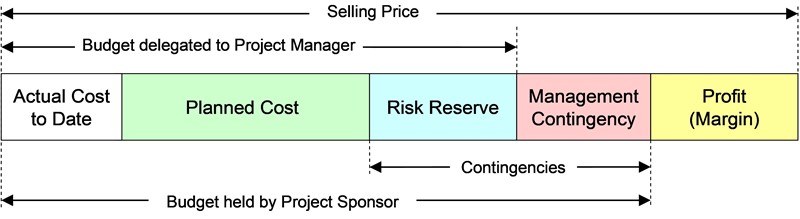

The figure below illustrates a typical approach to budgeting for project risk. Note that:

- Different terminologies may be used e.g. Risk budget instead of Risk Reserve.

- The Profit element is only relevant if the project is being delivered on a commercial basis. It would not usually be relevant to an internal or a government-owned project.

- The delegation of budgets may vary from that shown e.g. the sponsor may retain some of the Risk Reserve or Management Contingency may be pooled with other projects.

The Planned Cost is usually calculated deterministically from the project’s project plan and cost breakdown. Although, the Project Manager may delegate responsibility for elements of the planned cost to members of the project team, they retain overall accountability for actual costs relative to planned costs. As the project progresses, the Actual Cost will increase, whilst Planned Cost, Risk Reserve and Management Contingency should (normally) reduce.

The Risk Reserve may be used or delegated by the project manager to fund new risk responses and/or absorb the effects of risk as they occur. Its value should be derived from risk analysis – see the Cost Risk Analysis guidance sheet (August 2023). It should be based on the implications of risks owed by the project and the tolerance of risk by the organization.

Some organizations use “post-mitigation” estimates to calculate Risk Reserve. See the Pre and Post-mitigation Estimates guidance sheet (Sep 2022) for information on the issues involved.

More…

To read entire article, click here

Editor’s note: This series of articles is by Martin Hopkinson, author of the books “The Project Risk Maturity Model” and “Net Present Value and Risk Modelling for Projects” and contributing author for Association for Project Management (APM) guides such as Directing Change and Sponsoring Change. These articles are based on a set of short risk management guides previously available on his company website, now retired. For an Introduction and context for this series, click here. Learn more about Martin Hopkinson in his author profile below.

How to cite this paper: Hopkinson, M. (2023). Budgeting for Cost Risk: A brief guide, Practical Project Risk Management series, PM World Journal, Vol. XII, Issue IX, September. Available online at https://pmworldlibrary.net/wp-content/uploads/2023/09/pmwj133-Sep2023-Hopkinson-budgeting-for-cost-risk-risk-management-article.pdf

About the Author

Martin Hopkinson

United Kingdom

![]()

Martin Hopkinson, recently retired as the Director of Risk Management Capability Limited in the UK, and has 30 years’ experience as a project manager and project risk management consultant. His experience has been gained across a wide variety of industries and engineering disciplines and includes multibillion-pound projects and programmes. He was the lead author on Tools and Techniques for the Association for Project Management’s (APM) guide to risk management (The PRAM Guide) and led the group that produced the APM guide Prioritising Project Risks.

Martin’s first book, The Project Risk Maturity Model, concerns the risk management process. His contributions to Association for Project Management (APM) guides such as Directing Change and Sponsoring Change reflect his belief in the importance of project governance and business case development.

In his second book Net Present Value and Risk Modelling for Projects he brought these subjects together by showing how NPV and risk modelling techniques can be used to optimise projects and support project approval decisions. (To learn more about the book, click here.)

To view other works by Martin Hopkinson, visit his author showcase in the PM World Library at https://pmworldlibrary.net/authors/martin-hopkinson/